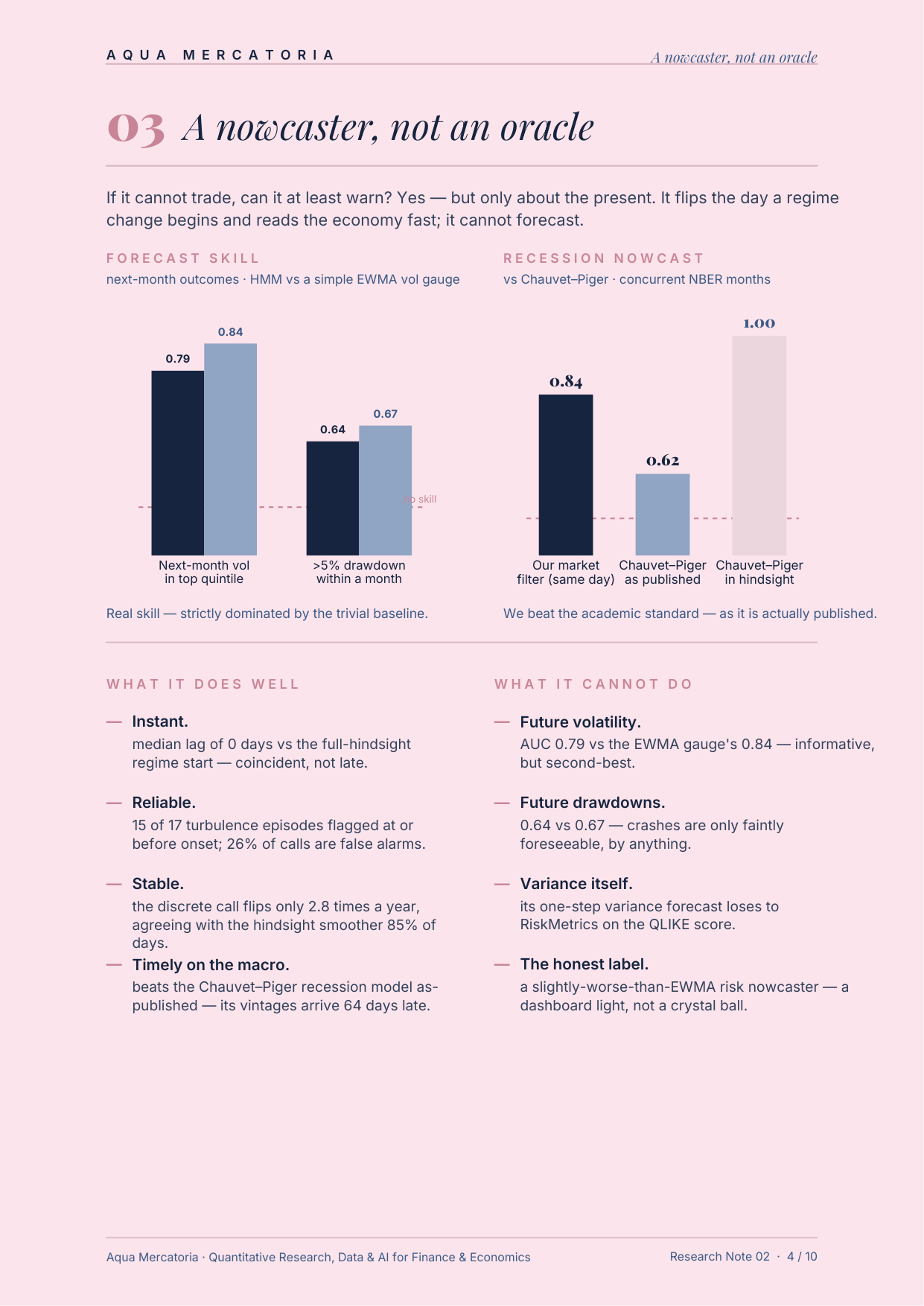

A market-regime research project testing whether models can distinguish real investment signal from backtest illusion.

Using tools such as Hidden Markov Models, walk-forward testing, point-in-time data, and simple baselines, Sentinel studies when markets shift from calm to stressed conditions — and what that actually means for investors.

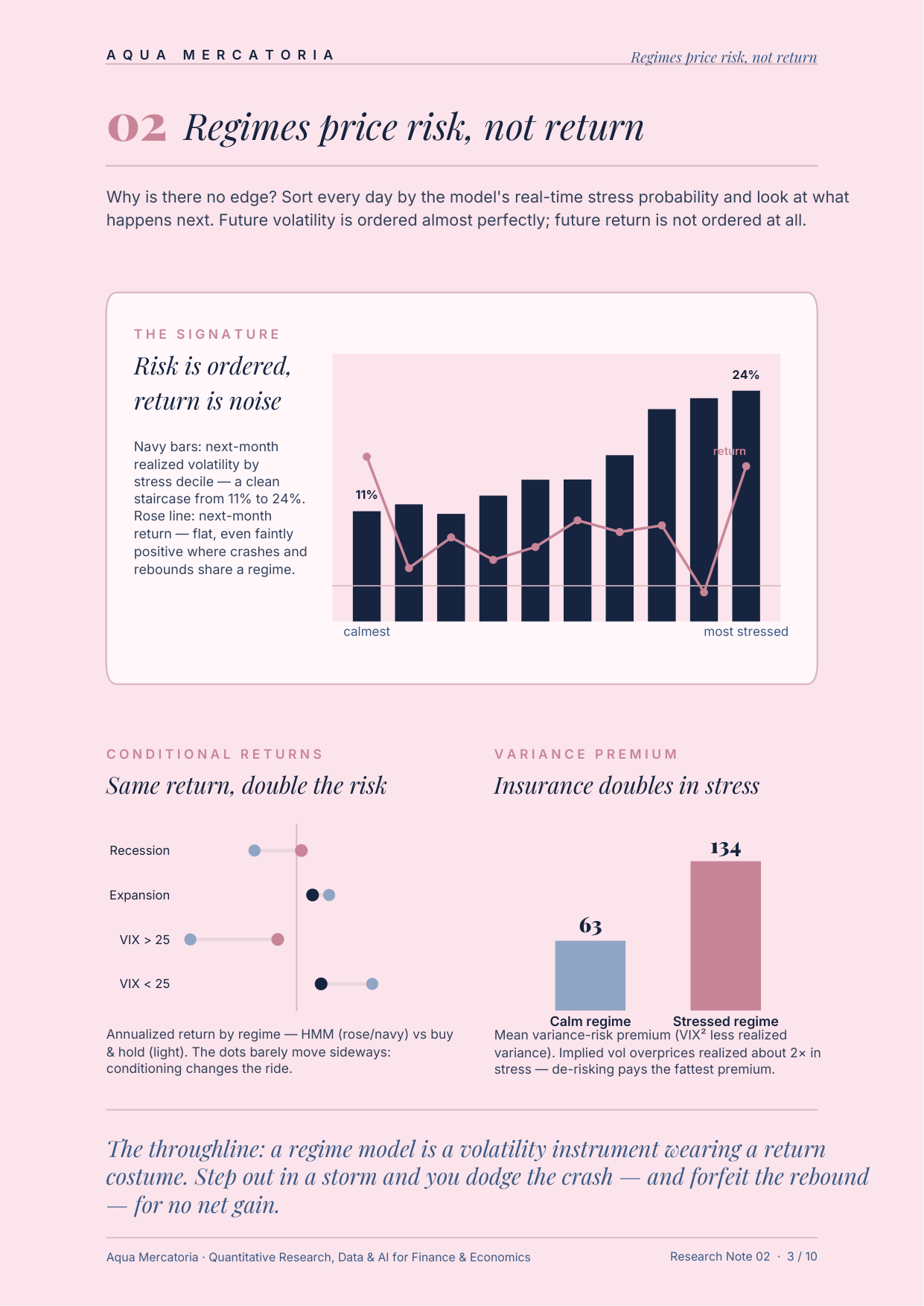

The core finding: regimes do not reliably predict returns. They reprice risk.

Sentinel is not designed as a magic trading signal, but as a risk overlay: a way to understand volatility, drawdown risk, and changing market conditions with more discipline.